Introduction

Recent years have witnessed an acceleration of sustainability agendas of banking systems around the world, particularly through the integration of climate risk management frameworks in the banking system.

This improvement became crucial due to the noticeable impacts of climate change on financial portfolios and the inadequacy of traditional risk management practices in identifying and responding to such idiosyncratic risks.

This movement was initially more prominent in Europe and the United Kingdom, then rapidly spread to other jurisdictions such as Australia, Canada, Singapore, and more recently the United States.

While banks made significant progress in recent years, climate risk consideration is still a novelty and evolves at different rates depending on the capabilities and challenges of these jurisdictions such as continuing methodological and data constraints.

In this article, we reflect on what to expect in future development of climate risk management in banking, based on emerging trends in European and UK climate risk stress testing and scenario analysis, as well as implications for the role of regulators.

Climate Risk Stress Testing and Scenario Analysis

Europe

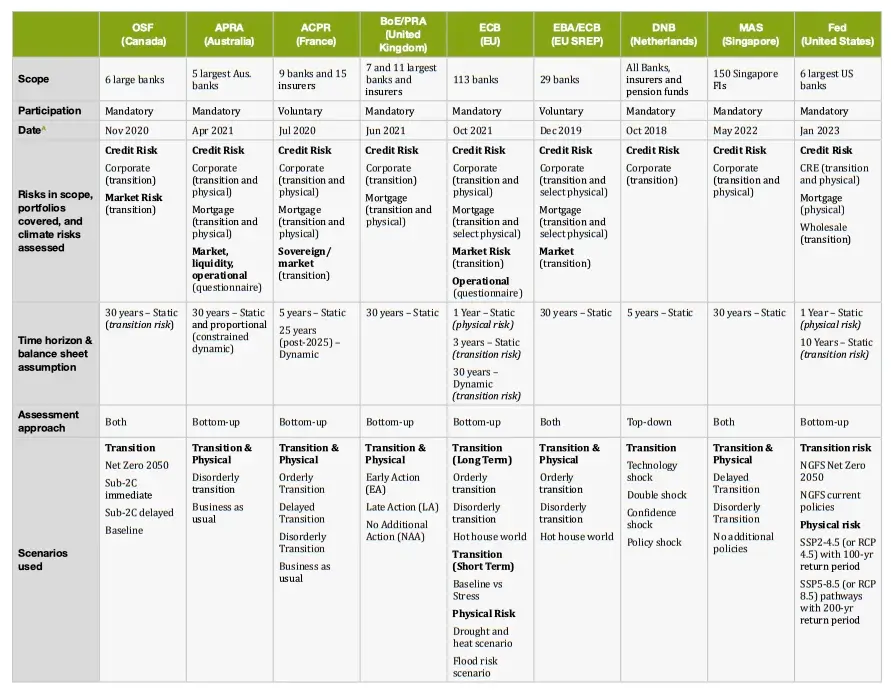

EU banks have actively participated in climate risk assessments, with the 2022 ECB stress test serving as a global benchmark. This exercise revealed varying capabilities, particularly in data management and risk scope.

The Association for Financial Markets in Europe (AFME) states that banks need a better understanding of physical risk channels and improved data governance for long-term risk forecasting.

Over 87% of banks are proactively addressing climate change through annual internal stress tests and scenario analyses. Most are keen to assess climate impacts on their portfolios, especially credit (100%) and market risk (67%), and there’s a growing interest (20%) in exploring other risk types like reputational and funding risks.

While 60% of banks lack a fully integrated climate risk framework, most plan to incorporate physical and transition risks over time. However, banks often underestimate risks, with 96% having identification blind spots, according to the ECB.

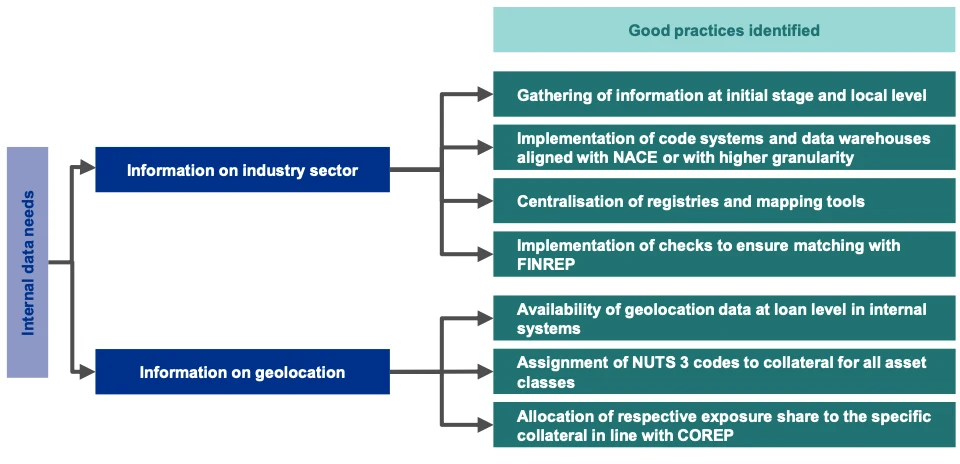

The EU supervisor later issued a good practice guide to aid banks in enhancing their climate risk assessment capabilities by 2024, hammering particularly on better approaches to build solid internal data (income splits, NACE 2 industries, GHG emissions, NUTS 3 geography) to accurately assess exposures, as banks resorted to external data providers.

In addition, the ECB continues to be a key contributor to the work of the NGFS in providing support to optimise scenario design and analysis.

As emphasised by Christine Lagarde, President of the ECB, “This workstream offers an invaluable climate risk assessment tool that provides policymakers globally with essential guidance. Furthermore, we chair the NGFS Experts’ Network on Legal Issues”.

In addition, the European Central Bank (ECB) has set a deadline for banks under its supervision to fully incorporate climate-related and environmental risks into their risk management practices by the end of this year, warning laggards with sanctions.

Internal Data Needs, Summary of Good Practices identified. Click the picture to expand. Source: ECB.

UK

Similarly, results from the UK’s Climate Biennial Exploratory Scenario (CBES) published in 2022 show that UK banks have made significant progress in incorporating climate risk into their current risk management systems and reporting mechanisms, but they face challenges in risk quantification, with a focus on key business areas and a reliance on third-party modelling capabilities.

Progress in risk appetite and risk evaluation has been notably hindered by the absence of standardised, high-quality data necessary for measuring, assessing, and modelling climate-related risks.

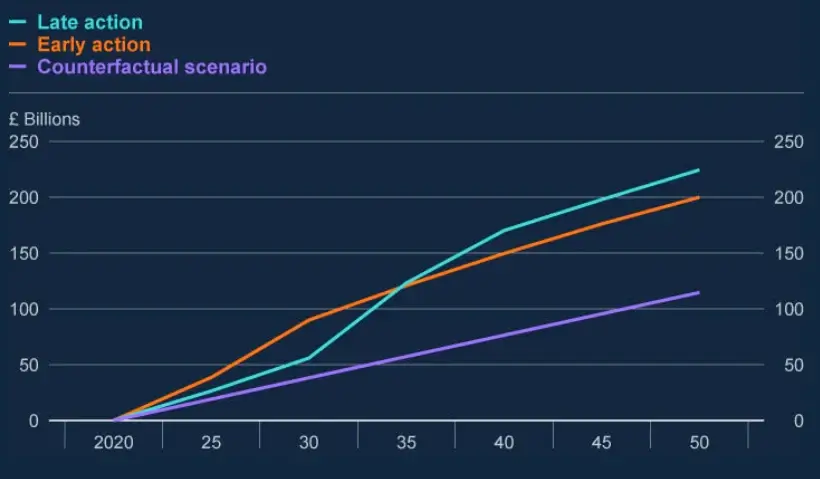

From what was analysed however, forecasts were concentrated solely on actual credit losses. While in all scenarios loss rates were expected to increase significantly, the highest projected credit losses for banks were in the Late Action scenario, where loss rates more than doubled due to climate risks.

This equates to approximately an additional £110 billion in losses over the period, with around 40% materialising during the initial five years of transition.

Like the EU, the UK has been working to improve future climate risk assessment exercises. This effort involves coordinated actions between various stakeholders, including banks, UK regulators, the UK Government, and external parties such as climate scientists.

One of the main channels for this coordination is the NGFS (Network for Greening the Financial System) pipeline. The insurance sector also plays a significant role in these efforts.

The Climate Financial Risk Forum (CFRF) provides guidance on these initiatives. The CFRF focuses on setting future data and research priorities. Key priorities include obtaining reliable and consistent counterparty data, as well as developing transition and adaptation plans.

Looking in the same Direction?

This indicates that European and UK jurisdictions are likely to remain a leading force to explore areas of progress and improve climate risk assessment capabilities in future stress testing and scenario analyses nationally and regionally.

To achieve this, regulators from both jurisdictions will potentially further collaboration, as they already work under similar international workstreams such as the NGFS, and the Basel Committee on Banking Supervision (BCBS).

Furthermore, the ongoing Project Gaia, though primarily a European-led initiative under the Bank of International Settlement (BIS), will serve as a major avenue to align UK and EU efforts to facilitate an in-depth assessment of climate-related risks in the financial system, leveraging on artificial intelligence (AI), specifically large language models (LLMs).

However, the project faces certain challenges:

- Data Standardisation: The complex landscape of regulations, frameworks, and standards has led to inconsistent reporting practices and data, limiting the usability and comparability of available information.

- Technical Challenges with LLMs: Integrating LLMs into applications for data extraction poses several technical challenges, including long response times, randomness (non-repeatability) in their outputs, and hallucinations, where the model generates information absent in the input data.

Data management in climate risk assessments is a major challenge for both the UK and the EU.

Despite these challenges, it is important to note that efforts are converging towards similar needs even though globally-aligned initiatives are not yet fully satisfactory.

Future inputs should emerge from:

- A deeper synergy between central banks within international climate risk workstreams, to effectively coordinate efforts to eliminate existing complexities of regulatory landscapes, frameworks and standards, and to break limitations to access available and credible data.

- A continuing engagement of banks and supervisors with climate risk data and scenario providers to provide best-in-class climate risk data analytics, and scenarios design and guidance.

Takeaways

- The EU and UK will remain at the forefront of integrating climate risk into banking through comprehensive stress testing and scenario analysis.

- Despite progress, both jurisdictions need improved data governance and modelling to overcome challenges in data standardisation and risk quantification, with future efforts likely focusing on developing high-quality data.

- International initiatives like Project Gaia highlight AI's potential for climate risk analysis and the need for innovation and international cooperation to overcome technical challenges and data limitations.

Physical Risk Data

Climate risk data is crucial to assess the long-term effects of climate change and enable stakeholders to develop informed adaptation strategies. These strategies could include enhancing building resilience or revising insurance policies, which help maintain property values and contribute to the overall stability of the property market.

You can estimate the asset-specific financial losses from both acute and chronic physical hazards with Spectra, the climate risk platform developed by Climate X. Plus, the innovative Adapt module allows you to determine the ROI of taking pre-emptive climate adaptation action based on a range of 22 different interventions.

{kind=link}

{kind=link}

{kind=link}