TL;DR

- Climate change critically threatens real estate market stability in the U.S. and Canada, affecting property values and mortgage lending with a few differences in terms of magnitude and severity.

- Although U.S. and Canada face escalating climate-related impacts that lead to significant property devaluation in high-risk areas, Canada's strict regulations help lessen some impacts but still see depreciation in disaster-prone regions.

- As climate risks drive higher down payments and interest rates in high-risk areas, both U.S. and Canadian lenders are at an early stage of integration of these risks, with the U.S. showing more advanced progress in integrating these assessments.

With record-breaking temperature rises looming, climate change is becoming a critical threat to the stability of the real estate market, challenging its traditional risk identification, adaptation, and mitigation practices globally.

The United States and Canada share some similar physical climate risks due to their geographical proximity, though specific risks like floods, hurricanes, and wildfires vary in intensity and occurrence based on regional climate, geography, and local factors.

These increasing risks present significant challenges for real estate valuation in both countries. This article investigates the impact and implications of climate risks on property values and mortgage lending in the U.S. and Canada.

Impact and Implications for Property Values

In the United States, property valuations are increasingly affected by escalating climate-related incidents such as hurricanes, wildfires, and floods.

According to the Sierra Club, in 2021, researchers found that houses in flood zones around the U.S. were overvalued by $44 billion; by 2022, the actuarial firm Milliman estimated it at $520 billion, representing unpriced flood costs.

Coastal regions, particularly in Florida, California, and Texas, face significant impacts from rising sea levels and amplified storm activities, leading to higher insurance expenses and diminished market values as these risks are factored in by buyers and investors.

For example, flood insurance premiums have doubled in 12 states, with rates in Florida surging by 231%, according to Inside Climate News.

Wildfire-prone areas like California have also seen notable reductions in property values due to repeated devastation and escalating reconstruction costs.

CoreLogic reports that between June 2021 and May 2023, “the price of properties located within a fire perimeter actually declined by 0.64%. In contrast, properties located within one mile from the fire experienced price appreciation of 5.1%, while those situated one to five miles away saw a 7.21% gain”.

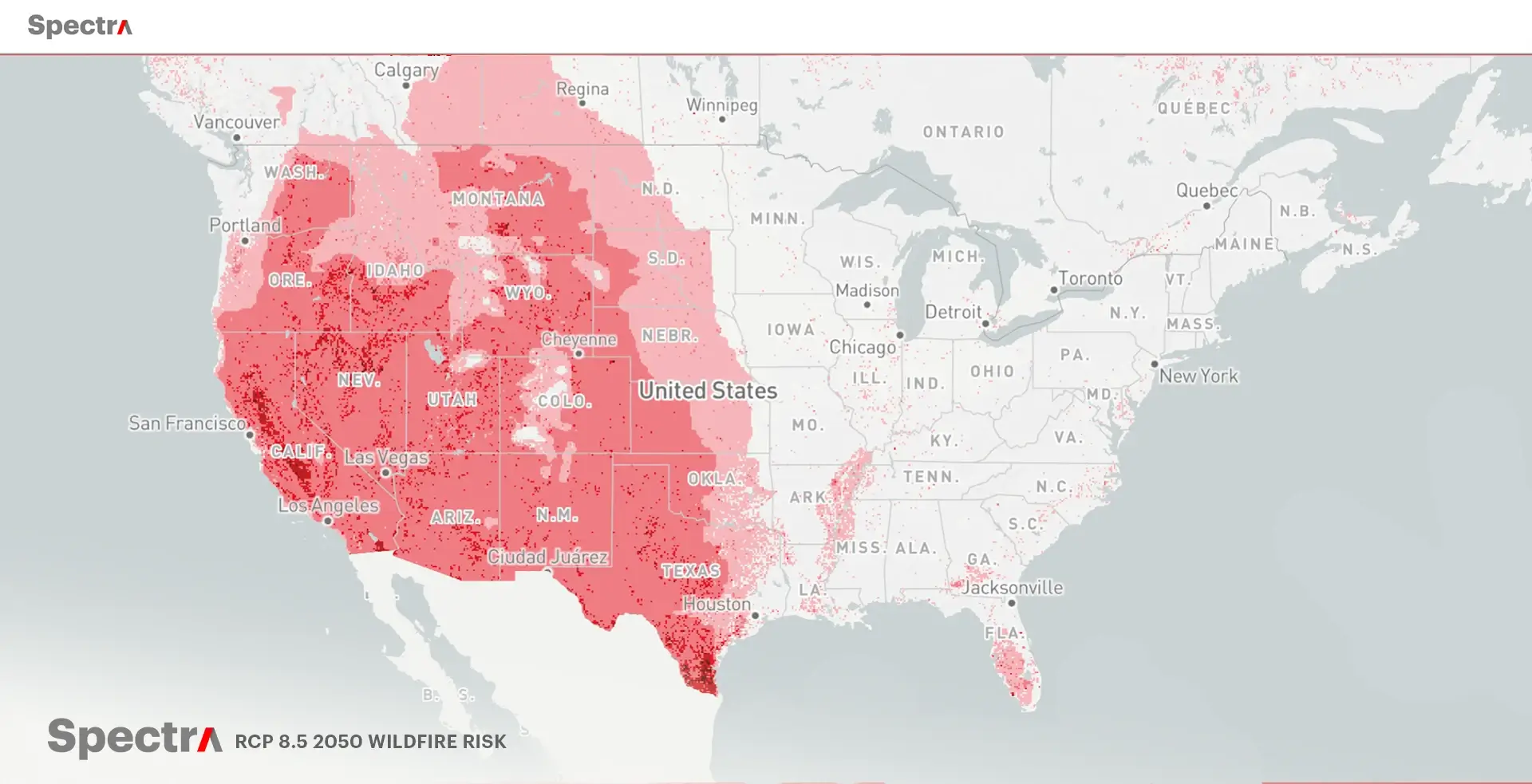

Spectra showcasing Wildfire risk in 2050 in the United States, using the "No Additional Action" RCP 8.5 scenario. Darker red indicates higher risk. Click the picture to expand.

Canada faces similar climate-related challenges, with coastal regions like British Columbia vulnerable to rising sea levels and flooding, and interior provinces facing increasing wildfire threats.

Professor Xu Yue from Nanjing University of Information Science and Technology highlights that, “owing to the distinctive topographical features of the Rocky Mountains, phase-locked related heat is more prone to occur in west-central Canada, consequently heightening the risk of intensified wildfire events”.

However, Canada's stringent building codes and regulations, such as the National Building Code of Canada (NBC) and the National Energy Code of Canada for Buildings (NECB), help mitigate these impacts.

These rules appear more rigorous than those in the U.S. Properties constructed to endure severe conditions and may result in maintaining positive property values better.

Unlike the U.S., Canada updated its building codes to support climate change adaptation and increase the resilience of buildings and infrastructure, including among other aspects the 2021-2026 Climate Resilient Built Environment (CRBE) Initiative.

Despite these measures, regions recurrently affected by disasters, like Fort McMurray, still experience significant property depreciation.

For instance, wildfires caused a significantly decline in residential real estate market in the region between October 2022 and October 2023: the average residential price in Fort McMurray has seen a decrease of approximately 16%, dropping from around $336,000 in October 2022 to about $282,000 in the same month in 2023.

The cost of a single-family home, which was over $700,000 about ten years prior, stood at $467,848 in 2023.

Impact and Implications for Mortgage Lending

In the U.S., there is a growing trend among mortgage lenders to include physical and transition climate risk assessments in their lending criteria, using prescribed scenarios analysis techniques from the IPCC, NGFS, IEA, supervisory stress test and regulatory climate-related financial disclosures.

In high-risk areas, lenders often require larger down payments or higher interest rates to counterbalance potential property value depreciation and increased default rates.

Eddie Seiler, executive director of the Research Institute for Housing America at the Mortgage Bankers Association, claims that “If you are underwriting a 30-year loan on a property at the Outer Banks of North Carolina, which will likely be washed into the ocean in 10 years, it needs to be taken into account very explicitly […] we’re not there yet as an industry”.

Homeowners in high-risk areas face challenges in meeting mortgage obligations due to climate-related damages and elevated insurance expenses, with severe scenarios leading to properties not recovering at all.

Properties in flood-prone areas like Miami have seen significant insurance premium increases, affecting homeowners' ability to maintain mortgage payments, as highlighted by the Herald, where flood rates in Key Biscayne may reach $7,000 annually.

If these compounded effects are not accurately measurable, they will not only continue to reflect a higher risk of damages and losses over time, but also compromise the effectiveness of climate risk management initiatives in place.

As a result, entities like Fannie Mae and Freddie Mac in the secondary mortgage market are also beginning to incorporate climate risk into their securitisation processes, potentially leading to a wider re-evaluation of mortgage-backed securities (MBS) in regions vulnerable to climate change.

By integrating climate risk assessments, these entities can better evaluate the long-term viability of the mortgages they purchase and bundle into securities.

This process could involve scrutinising the geographic and environmental vulnerabilities of the properties underlying the mortgages and based on forward-looking data, which could in turn provide more accurate results and better assumptions and predictions.

Canadian mortgage lenders, on the other hand, are also starting to consider climate risks in their lending decisions, particularly concerned about the abundance of “poor disclosure practices” in real estate sector, although the process is not as advanced as in the U.S..

Known for their conservative lending practices, Canadian banks are starting to develop more comprehensive risk assessments considering properties in high-risk areas, while also acknowledging challenges to incorporate physical risk elements due to limitations to manage physical risk data, and to understand and translate physical impacts into financial costs.

The Canadian Mortgage and Housing Corporation (CMHC) has begun to consider climate risks as part of their wider risk management strategy.

Unlike in the U.S., where the market is dominated by private insurers, the presence of CMHC provides a safety net, but it also implies that systemic risks could have wider implications for the national housing market.

Physical Risk Data

Climate risk data is crucial to assess the long-term effects of climate change and enable stakeholders to develop informed adaptation strategies. These strategies could include enhancing building resilience or revising insurance policies, which help maintain property values and contribute to the overall stability of the property market.

You can estimate the asset-specific financial losses from acute and chronic physical hazards with Spectra, the climate risk platform developed by Climate X. Plus, the innovative Adapt module allows you to determine the ROI of taking pre-emptive climate adaptation action based on a range of 22 different interventions.

{kind=link}